Everybody wants to save money, whether it be for that dream vacation, investing to get rich, or to own your own home.

In this post we will discuss some common techniques for saving money and getting control over your finances.

Even though it’s true that money can’t buy happiness, it can guarantee a roof over your head, food on the table, and clothes on your back. This goes a long, long, way in achieving happiness. The techniques discussed in this article are not mutually exclusive and we recommend you use multiple for the best results.

Technique 1: Categorize your Spending

All expenses can be categorised into either a Necessity OR a Comfort OR a Luxury.

Necessities are payments that you cannot avoid and/or need to survive. This could include expenses such as:

- Groceries

- Rent

- Loan repayments

- Electricity

- Water bill

- School fees

Comfort Expenses Add To Your Comfort, Or Many Have Entertainment Value

This could include cosmetics or streaming services. This could also include eating meals out where making your own food is cheaper.

Luxury Costs Are Not Essential And May Be Beyond Your Income Level

These are expenses that are not essential at all and provide less value to your life than comfort expenses. This could include expensive watches, clothes, upmarket restaurants, luxurious vacations etc.

How certain expenses are categorised may depend on your own situation; if you live in a city with reliable and clean public transport, then a private vehicle and its related expenses are a comfort and not a necessity.

Generally, you want to eliminate luxury expenses from your spending and reduce comfort expenses. Note that if you are financially comfortable, reducing these expenses may not be the best course of action. If you are not spending money on some comfort expenses, it may take a toll on your mental health.

Technique 2: – Use Excel For Budgeting

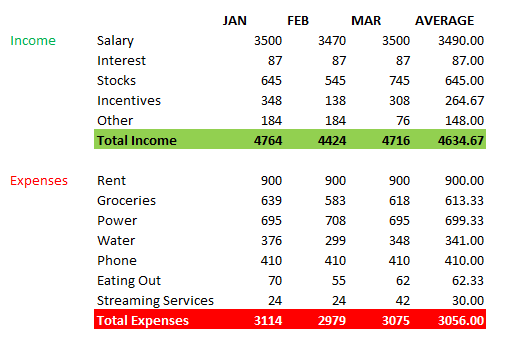

Excel is a common budgeting tool because of the intuitive function and widespread use. There are many templates available online, but another benefit of excel is the customisability and flexibility. This enables you to decide how you want to track your spending. For a very simple idea, see below.

Create an Excel sheet, list all your income and expenses in it. You may want to group some expenses together e.g., instead of having individual expenses for each time you ate out, just have one ‘eating out’ category. It is generally easiest to track this over the course of a month.

Based off these numbers you can estimate how much you are spending and on what. Use this as a guide when you make your budget and spending goals.

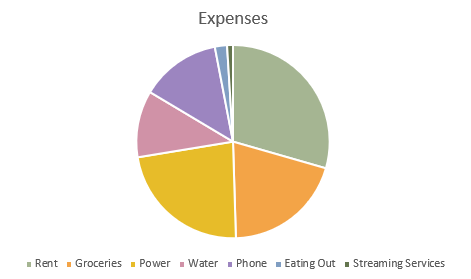

Another great feature of excel is the ability to create visualizations. Here is a pie graph for the average expenses.

This is incredibly useful as people process visual information much easier than written and this process will give you a holistic picture of where your money is going.

Technique 3 – Little Expenses Add up

In a study conducted in the US, the biggest energy consuming devices were air conditioners, with the second being cable TV set-top boxes. Given the skyrocketing cost of energy bills, reducing your energy usage is a hopefully easy way to shave a few dollars off.

Turn off appliances when they are not in use and reduce your usage of heating and cooling systems where possible. Supermarkets are generally laid out as follows: Basic items such as meat, fruit and veg, and bakery items are on the outside of the aisles and snacks etc. are on the inside.

To reduce your grocery bill, stick to the outside ring. It is also very beneficial to plan your meals in advance so that you buy only what you need. Who knows, maybe avoiding some of the more costly processed food in the aisles will save you money on health bills in the long term!

Basic foods such as whole grain and raw foods not only cost less but have health benefits that result in savings in your medical bills. Avoid eating out as it is costly. Pack your lunch at home and avoid food delivery apps – uninstall them if you need to.

We are constantly exposed to marketing for new and expensive products that try to convince us that owning this product will enhance your life. Products such as these are not worth it and will become “regret purchases”.

If you see something you really like, wait a week. If you still really love it and can picture yourself using it enough to add value, buy it! Budgeting doesn’t have to mean sacrificing everything, just being prudent.

Try to find the best deals for your phone, internet, and insurance bills etc. Renegotiate wherever you can – it may feel awkward but think about what that money could mean down the line. That could be a nice holiday, or a birthday present

Remove all subscriptions and TV channels that you don’t use frequently enough to justify. Unsubscribe to newspapers/magazines/publications that you don’t read, relinquish club memberships that you rarely use. Be realistic about your usage of subscription-based products – are you really using it enough to justify the cost?

Technique 4 – Loan Restructuring And Change In Spending Habits

Restructure your loans, credit cards and mortgages. Relinquish the cards that you don’t use. Put money in a savings account and spend from it, instead of taking credit and repaying it later.

Using credit cards for common expenses is dangerous, and debit cards will not let you spend beyond your means. Use Debit cards and pay only what you already have. Moreover, some savings accounts encourage you to round off your transaction and the change goes to a higher rate fixed deposit.

Technique 5 – Set Long Term And Short-term Goals To Keep Yourself Motivated

Start daydreaming and remind yourself about a few things you longed for.

Setting a goal lets you plan an effective strategy and keep an eye of where you’re headed.

Your Short-term goals could be – create an emergency fund (3-6 months of your monthly expenses), get rid of all debts, increase your disposable income, pay off your car loan, be able to afford a vacation.

Your Long-term goals could be – save enough for your retirement, your children’s’ education, a bigger home etc.

Every month, assess if you’re heading towards your goals or not.

Also, adjust your estimates if needed, based on new information or changes that have occurred.

Goal Setting will keep you focussed, motivated and a bit relaxed about your financial future, as you know you’re following the right path.

The techniques and tips listed here are a sure-fire start to the budgeting and saving process. Following them will reap rewards.